Flat Rate 'Commodity' Pricing Is Wrong *For Some

FEbruary 22, 2026– Michael Marsh

I've read much by Joe Paduda (literally every blog he writes). This article is an update to the one published on March 13, 2017, Flat Rate Pricing Increases Costs. I said at the time that, while we may diverge on opinions at times, I am in total agreement with a blog post by Joe Paduda from the perspective of a workers’ compensation Third Party Administrator.

In an article published on October 12, 2023, Mr. Paduda expands upon the increasing commoditization of claim services @ https://www.joepaduda.com/2023/10/12/work-comp-services-the-commodity-trap-and-avoidance-thereof/ and how workers' compensation claims administration is and has been sold to service buyers as a commodity.

He writes:

"This is NOT unique to bill review...lazy buyers and brokers/consultants usually commoditize claims, networks, clinical services, occupational medicine, Medicare Set Asides and other services.

Why? Because it is easy, requires little effort, and, frankly, vendors fail to focus on value. Rare indeed is the service company that really, really trains its sales folks, or invests in market research, or has any concept of branding.

So, yeah, it’s on the vendors too. If you – the service provider – don’t fully understand what your customers value AND are able to clearly and crisply articulate how your company can deliver that value, you’re forever going to compete on price."

Having been working in the claims area since junior high school, with Midland Claims our now 3 generation as an independent claims business, I've been blessed (some might say cursed) to see the changes in the claims industry over these 50+ years. My experience also included a 14 year stint in California where I managed the 38 state home office claims operations of two insurance companies. I've been truly blessed to be on both sides of the payer / service provider part of the business of claims. My observation: commoditization of claims 'services' began a very long time ago.

In the 1960's and 1970's, much of the claims field work for all P & C lines of insurance, commercial, personal and workers' compensation, were handled by a combination of company adjusters and independents ("IAs"). In Montana, there were very few company adjusters. So few in fact that Midland Claims had extensive relationships with many carriers such as State Farm, GEICO, and Liberty Mutual. I'll never forget watching my father sign State Farm and Government Employees claim checks and (face-to-face) exchanging them for Releases and Proof of Loss forms.

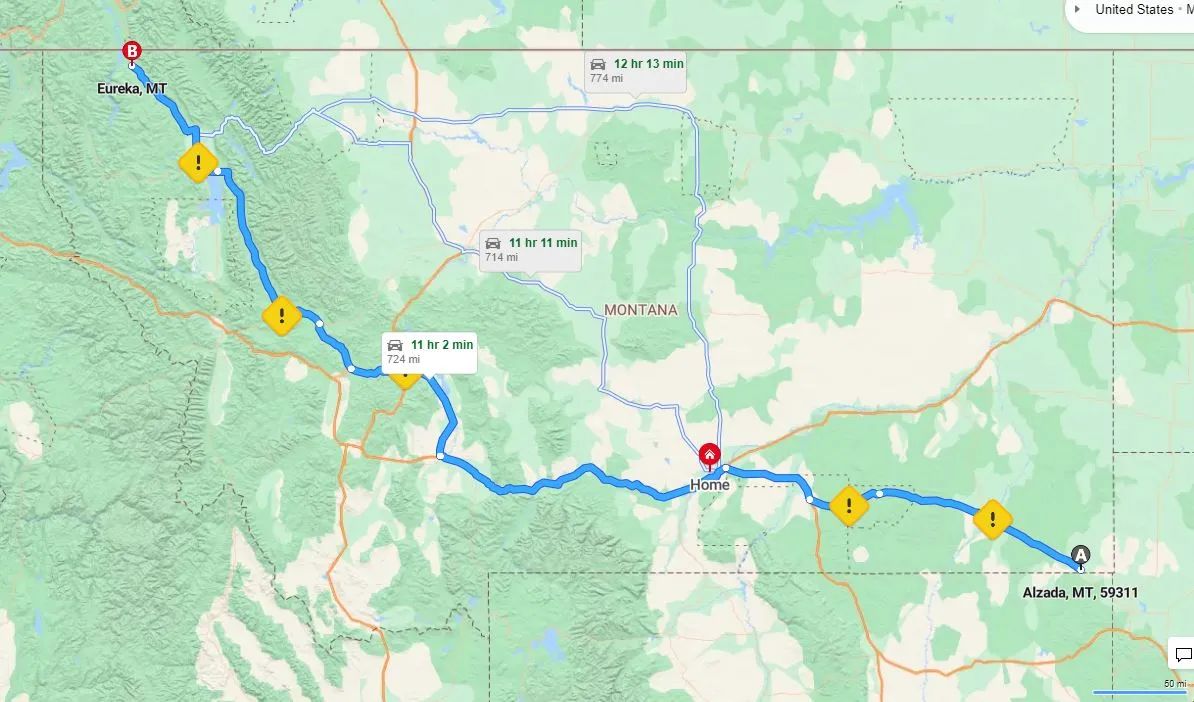

We in Montana saw the trend of consolidation before most other states. We were the "sparrow in the coal mine" as the saying goes. Our focused service territory is the state of Montana, a sparsely populated but geographically massive state. We received the distinction in the last census, there were found to have more than 1,000,000 residents of the state...first time ever in history. Geographically, Montana is the 4th largest in the United States:

- Alaska: 663,267 square miles (1,717,854 sq km)

- Texas: 268,820 square miles (696,241 sq km)

- California: 163,695 square miles (423,968 sq km)

- Montana: 147,042 square miles (380,837 sq km)

For example, the drive from Alzeda, MT to Eureka, MT is 724 miles, or approximately 11 hours...one way. I routinely get calls, usually from Eastern states, asking if we will conduct a limited assignment in Missoula, Whitefish or Great Falls (cities in central and Western Montana). Only once in almost two decades has an insurance company or out of state TPA given us such an assignment...the cost of ten plus hours of drive time has been the limiting financial factor. Those claims are then handled by the payer directly using cell phone photos, virtual data drives and zoom-type services for the claims person to work directly with their insured customer or the injured third party indiviudal.

So one might ask, what does this have to do with commodity pricing of services in the workers' compensation claims space? As generations of experienced adjusters, examiners and claims managers move on to the more relaxed time of life (retirement), a bit of institutional knowledge is lost. Just a pebble for each, thousands of pebbles industrywide. With generational influences present today that were less prevalent a few decades ago, the thinking has shifted to one more in the realm of simplicity, convenience and digital connection.

Value is measured two ways.

One is to highlight and celebrate the simplicity of one national claims TPA agreement, obtained using a very basic claim service pricing model...many times the payment to the claims TPA is based solely upon a flat rate per claim. There is no allowance for ancillary services such as medical bill review, medical case management services and Vocational Rehabilitation vendor charges.

The second is to include all costs associated with the program, including the charges above, legal expense, cost of excess workers' compensation insurance or reinsurance and, importantly, the cost of loss. This tends to be a more holistic approach to managing a workers' compensation program. In such program approaches, each state, each separate jurisdiction, should be evaluated separately and independently to ensure the highest quality service provided at the lowest possible total cost.

In approach one, the TPA evaluation process is relatively simple and quick. Who offers the lowest unit price and passes the basic due diligence test is normally the winner of the chicken dinner. And internally, the entire process can be handled by non-workers' compensation claims experienced staff in a remote purchasing department. They don't need to know the variables of the system in California versus Oklahoma versus Idaho. They are incentivized to obtain the lowest cost per claim. Spreadsheet analysis at its finest.

Approach two is far more complicated and requires a much higher level of internal staff involvement in the evaluation and decision making process. These people need to know the jurisdictional differences, the friction (and costs) associated with those differences and understand the concept of the finger in the balloon. That concept is simple: When you push your finger into a balloon filled with water (reducing claims TPA unit cost), the displacement will appear elsewhere on the balloon through either general or pinpoint expansion. It is an action/reaction that cannot be avoided much like gravity. We might not see it or understand it, but it still holds us down. You can't change gravity. And you can't change cost transfer.

The challenge that is so often misunderstood with the cost transfer on the claims TPA cost balloon is that it is not generally a one to one relationship. When unit costs are brought down unrealistically, the increases in ancillary costs and losses paid are many times the savings used to validate the per claim pricing model. In approach one, those secondary cost increases are not tracked or even in the model. The incentive is purely to reduce the unit cost.

In other postings we have talked about the 'experiment'. This is where our single state workers' compensation claims practice refused flat rate pricing and solely worked with purchases of claims services that embraced the holistic cost method in approach two. We have taken claims over from Sedgwick, Gallagher, Crawford and others. In EVERY CASE there were significant full program cost savings. This took place over 35,000 claims and nearly $200 M in paid losses.

What value does a single state, single location independent Third Party Administrator in Montana or other states offer to its payer customers? The ability to handle workers' compensation claims in a jurisdictionally expert way while ensuring the lowest holistic program cost in each jurisdiction.

How does the value that the independent claims service provider fall into the vision of insurance company, captive and fronting operation claims service purchases? Simply stated, if the organization is procedurally tied to approach one, there is no synergy. We have passed, and been passed by, may potential claims service arrangements. Our experiment in providing claims services in the context of approach two has been a success...and it is a true blessing to be able to work with these fine organizations that appreciate and celebrate the big wins.

Back to Paduda, the interesting parallel between the medical cost per service pricing in the country is the same when the Purchasing Department, with no experience with workers' compensation claims nor any accountability for the overall cost of the program several years down the road, is tasked with handling the of acquisition of workers’ compensation TPA services. Flat rates have become the defacto standard. Seems as though without flat rates the Purchasing staff cannot do spreadsheet comparisons. They typically have no responsibility for the total cost of the program, they are only measured for the amount of 'savings' achieved through the RFP. This is driving claims services away from the adjuster / recovering worker relationship and towards ‘best practices’ which tend to serve as a lowest ‘measurable’ common denominator. When the bond between the adjuster/examiner and the recovering worker is broken, the total cost of the program rises significantly. I have seen this in every program that we have assumed at Midland Claims from other claims TPAs, and with many of my consulting clients' programs.

Takeaway: Cost per service does not work effectively with medical care, and works even less effectively than alternative methods of charging for professional claims services. Buyers of workers' compensation claims services should investigate claim service costs in the context of the full cost of the program. Simply saving on the TPA flat rate cost may actually be responsible for a significant holistic program cost increase..